支付卡欺诈检测的事件分类

作者: achoum

创建日期 2024/02/01

最后修改日期 2024/02/01

描述: 使用 Temporian 和前馈神经网络检测欺诈性支付卡交易。

此 Notebook 依赖于 Keras 3、Temporian 和其他一些库。您可以按如下方式安装它们

pip install temporian keras pandas tf-nightly scikit-learn -U

import keras # To train the Machine Learning model

import temporian as tp # To convert transactions into tabular data

import numpy as np

import os

import pandas as pd

import datetime

import math

import tensorflow as tf

from sklearn.metrics import RocCurveDisplay

引言

支付欺诈检测对于银行、企业和消费者至关重要。仅在欧洲,2019 年的欺诈交易估计就达到了 18.9 亿欧元。全球约有 3.6% 的商业收入因欺诈而损失。在本 Notebook 中,我们使用 Le Borgne 等人所著的《信用卡欺诈检测的可复现机器学习》一书附带的合成数据集,训练和评估一个模型来检测欺诈性交易。

欺诈性交易通常无法通过孤立地查看单个交易来检测。相反,欺诈性交易是通过查看同一用户、同一商家或其他类型关系之间的多个交易模式来检测的。为了以机器学习模型能够理解的方式表达这些关系,并通过特征工程增强特征,我们使用 Temporian 预处理库。

我们将交易数据集预处理成表格数据集,并使用前馈神经网络来学习欺诈模式并进行预测。

加载数据集

该数据集包含 2018 年 4 月 1 日至 2018 年 9 月 30 日期间抽样的支付交易。交易数据以 CSV 文件形式存储,每天一个文件。

注意:下载数据集大约需要 1 分钟。

start_date = datetime.date(2018, 4, 1)

end_date = datetime.date(2018, 9, 30)

# Load the dataset as a Pandas dataframe.

cache_path = "fraud_detection_cache.csv"

if not os.path.exists(cache_path):

print("Download dataset")

dataframes = []

num_files = (end_date - start_date).days

counter = 0

while start_date <= end_date:

if counter % (num_files // 10) == 0:

print(f"[{100 * (counter+1) // num_files}%]", end="", flush=True)

print(".", end="", flush=True)

url = f"https://github.com/Fraud-Detection-Handbook/simulated-data-raw/raw/6e67dbd0a3bfe0d7ec33abc4bce5f37cd4ff0d6a/data/{start_date}.pkl"

dataframes.append(pd.read_pickle(url))

start_date += datetime.timedelta(days=1)

counter += 1

print("done", flush=True)

transactions_dataframe = pd.concat(dataframes)

transactions_dataframe.to_csv(cache_path, index=False)

else:

print("Load dataset from cache")

transactions_dataframe = pd.read_csv(

cache_path, dtype={"CUSTOMER_ID": bytes, "TERMINAL_ID": bytes}

)

print(f"Found {len(transactions_dataframe)} transactions")

Download dataset

[0%]..................[10%]..................[20%]..................[30%]..................[40%]..................[50%]..................[59%]..................[69%]..................[79%]..................[89%]..................[99%]...done

Found 1754155 transactions

每笔交易由一行表示,包含以下重要列信息

- TX_DATETIME:交易的日期和时间。

- CUSTOMER_ID:客户的唯一标识符。

- TERMINAL_ID:进行交易的终端标识符。

- TX_AMOUNT:交易金额。

- TX_FRAUD:交易是否为欺诈交易 (1) 或非欺诈交易 (0)。

transactions_dataframe = transactions_dataframe[

["TX_DATETIME", "CUSTOMER_ID", "TERMINAL_ID", "TX_AMOUNT", "TX_FRAUD"]

]

transactions_dataframe.head(4)

| TX_DATETIME | CUSTOMER_ID | TERMINAL_ID | TX_AMOUNT | TX_FRAUD | |

|---|---|---|---|---|---|

| 0 | 2018-04-01 00:00:31 | 596 | 3156 | 57.16 | 0 |

| 1 | 2018-04-01 00:02:10 | 4961 | 3412 | 81.51 | 0 |

| 2 | 2018-04-01 00:07:56 | 2 | 1365 | 146.00 | 0 |

| 3 | 2018-04-01 00:09:29 | 4128 | 8737 | 64.49 | 0 |

数据集高度不平衡,大部分交易是合法的。

fraudulent_rate = transactions_dataframe["TX_FRAUD"].mean()

print("Rate of fraudulent transactions:", fraudulent_rate)

Rate of fraudulent transactions: 0.008369271814634397

将 pandas 数据框转换为 Temporian EventSet,这更适合后续步骤的数据探索和特征预处理。

transactions_evset = tp.from_pandas(transactions_dataframe, timestamps="TX_DATETIME")

transactions_evset

WARNING:root:Feature "CUSTOMER_ID" is an array of numpy.object_ and will be casted to numpy.string_ (Note: numpy.string_ is equivalent to numpy.bytes_).

WARNING:root:Feature "TERMINAL_ID" is an array of numpy.object_ and will be casted to numpy.string_ (Note: numpy.string_ is equivalent to numpy.bytes_).

| timestamp | CUSTOMER_ID | TERMINAL_ID | TX_AMOUNT | TX_FRAUD |

|---|---|---|---|---|

| 2018-04-01 00:00:31+00:00 | 596 | 3156 | 57.16 | 0 |

| 2018-04-01 00:02:10+00:00 | 4961 | 3412 | 81.51 | 0 |

| 2018-04-01 00:07:56+00:00 | 2 | 1365 | 146 | 0 |

| 2018-04-01 00:09:29+00:00 | 4128 | 8737 | 64.49 | 0 |

| 2018-04-01 00:10:34+00:00 | 927 | 9906 | 50.99 | 0 |

| … | … | … | … | … |

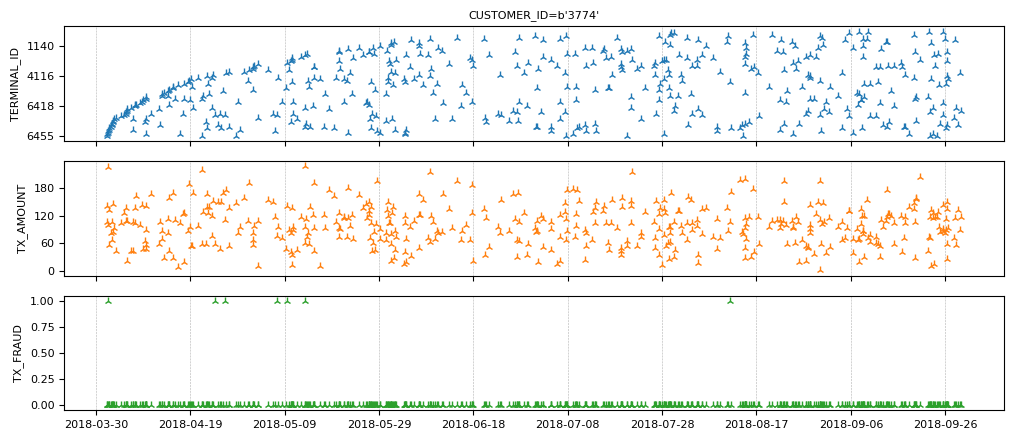

可以绘制整个数据集,但结果图将难以阅读。相反,我们可以按客户对交易进行分组。

transactions_evset.add_index("CUSTOMER_ID").plot(indexes="3774")

请注意此客户的少数欺诈性交易。

准备训练数据

欺诈性交易无法孤立地检测。相反,我们需要关联相关交易。对于每笔交易,我们计算同一终端在过去 n 天内的交易总额和数量。由于我们不知道 n 的正确值,我们使用多个 n 值并为每个值计算一组特征。

# Group the transactions per terminal

transactions_per_terminal = transactions_evset.add_index("TERMINAL_ID")

# Moving statistics per terminal

tmp_features = []

for n in [7, 14, 28]:

tmp_features.append(

transactions_per_terminal["TX_AMOUNT"]

.moving_sum(tp.duration.days(n))

.rename(f"sum_transactions_{n}_days")

)

tmp_features.append(

transactions_per_terminal.moving_count(tp.duration.days(n)).rename(

f"count_transactions_{n}_days"

)

)

feature_set_1 = tp.glue(*tmp_features)

feature_set_1

| timestamp | sum_transactions_7_days | count_transactions_7_days | sum_transactions_14_days | count_transactions_14_days | sum_transactions_28_days | count_transactions_28_days |

|---|---|---|---|---|---|---|

| 2018-04-02 01:00:01+00:00 | 16.07 | 1 | 16.07 | 1 | 16.07 | 1 |

| 2018-04-02 09:49:55+00:00 | 83.9 | 2 | 83.9 | 2 | 83.9 | 2 |

| 2018-04-03 12:14:41+00:00 | 110.7 | 3 | 110.7 | 3 | 110.7 | 3 |

| 2018-04-05 16:47:41+00:00 | 151.2 | 4 | 151.2 | 4 | 151.2 | 4 |

| 2018-04-07 06:05:21+00:00 | 199.6 | 5 | 199.6 | 5 | 199.6 | 5 |

| … | … | … | … | … | … | … |

| timestamp | sum_transactions_7_days | count_transactions_7_days | sum_transactions_14_days | count_transactions_14_days | sum_transactions_28_days | count_transactions_28_days |

|---|---|---|---|---|---|---|

| 2018-04-01 16:24:39+00:00 | 70.36 | 1 | 70.36 | 1 | 70.36 | 1 |

| 2018-04-02 11:25:03+00:00 | 87.79 | 2 | 87.79 | 2 | 87.79 | 2 |

| 2018-04-04 08:31:48+00:00 | 211.6 | 3 | 211.6 | 3 | 211.6 | 3 |

| 2018-04-04 14:15:28+00:00 | 315 | 4 | 315 | 4 | 315 | 4 |

| 2018-04-04 20:54:17+00:00 | 446.5 | 5 | 446.5 | 5 | 446.5 | 5 |

| … | … | … | … | … | … | … |

| timestamp | sum_transactions_7_days | count_transactions_7_days | sum_transactions_14_days | count_transactions_14_days | sum_transactions_28_days | count_transactions_28_days |

|---|---|---|---|---|---|---|

| 2018-04-01 14:11:55+00:00 | 2.9 | 1 | 2.9 | 1 | 2.9 | 1 |

| 2018-04-02 11:01:07+00:00 | 17.04 | 2 | 17.04 | 2 | 17.04 | 2 |

| 2018-04-03 13:46:58+00:00 | 118.2 | 3 | 118.2 | 3 | 118.2 | 3 |

| 2018-04-04 03:27:11+00:00 | 161.7 | 4 | 161.7 | 4 | 161.7 | 4 |

| 2018-04-05 17:58:10+00:00 | 171.3 | 5 | 171.3 | 5 | 171.3 | 5 |

| … | … | … | … | … | … | … |

| timestamp | sum_transactions_7_days | count_transactions_7_days | sum_transactions_14_days | count_transactions_14_days | sum_transactions_28_days | count_transactions_28_days |

|---|---|---|---|---|---|---|

| 2018-04-02 10:37:42+00:00 | 6.31 | 1 | 6.31 | 1 | 6.31 | 1 |

| 2018-04-04 19:14:23+00:00 | 12.26 | 2 | 12.26 | 2 | 12.26 | 2 |

| 2018-04-07 04:01:22+00:00 | 65.12 | 3 | 65.12 | 3 | 65.12 | 3 |

| 2018-04-07 12:18:27+00:00 | 112.4 | 4 | 112.4 | 4 | 112.4 | 4 |

| 2018-04-07 21:11:03+00:00 | 170.4 | 5 | 170.4 | 5 | 170.4 | 5 |

| … | … | … | … | … | … | … |

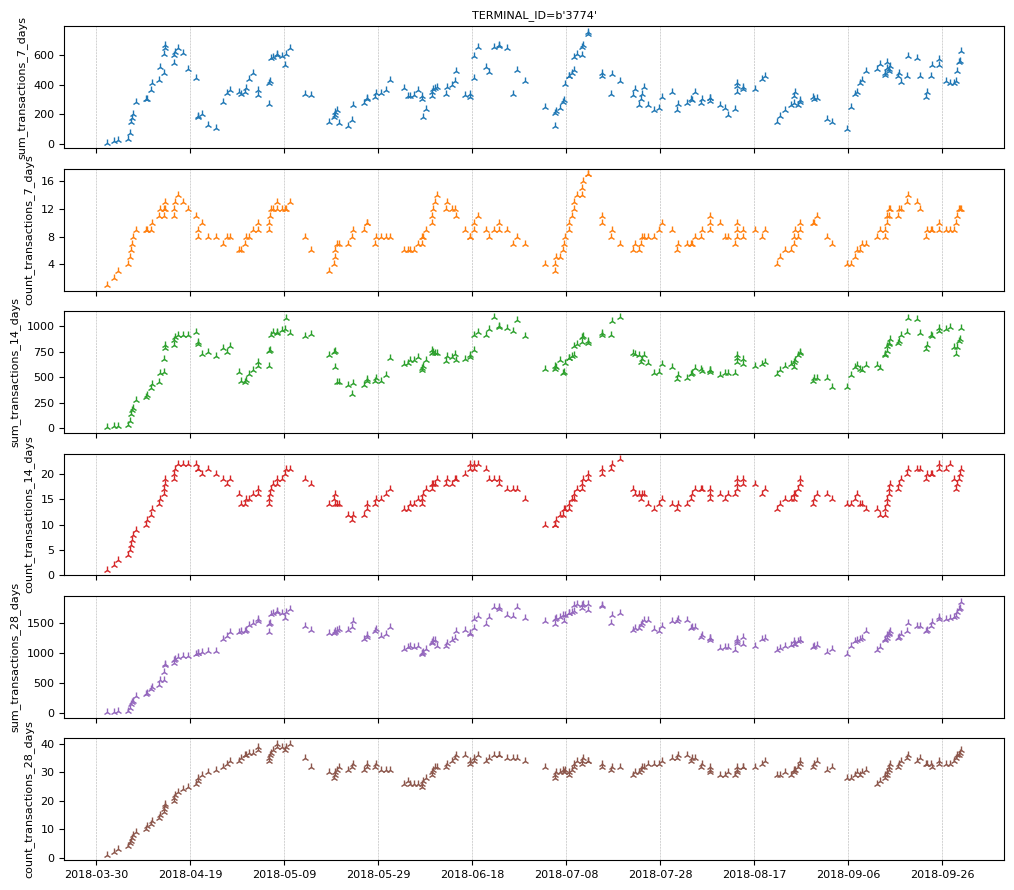

让我们看看终端 "3774" 的特征。

feature_set_1.plot(indexes="3774")

交易的欺诈状态在交易发生时是未知的(否则就不会有问题了)。然而,银行在交易发生一周后会知道交易是否为欺诈。我们创建了一组特征,指示过去 N 天内欺诈交易的数量和比例。

# Lag the transactions by one week.

lagged_transactions = transactions_per_terminal.lag(tp.duration.weeks(1))

# Moving statistics per customer

tmp_features = []

for n in [7, 14, 28]:

tmp_features.append(

lagged_transactions["TX_FRAUD"]

.moving_sum(tp.duration.days(n), sampling=transactions_per_terminal)

.rename(f"count_fraud_transactions_{n}_days")

)

tmp_features.append(

lagged_transactions["TX_FRAUD"]

.cast(tp.float32)

.simple_moving_average(tp.duration.days(n), sampling=transactions_per_terminal)

.rename(f"rate_fraud_transactions_{n}_days")

)

feature_set_2 = tp.glue(*tmp_features)

交易日期和时间可能与欺诈相关。虽然每笔交易都有时间戳,但机器学习模型可能难以直接使用它们。相反,我们从时间戳中提取各种信息丰富的日历特征,例如小时、星期几(例如周一、周二)和月中的日期(1-31)。

feature_set_3 = tp.glue(

transactions_per_terminal.calendar_hour(),

transactions_per_terminal.calendar_day_of_week(),

)

最后,我们将所有特征和标签组合在一起。

all_data = tp.glue(

transactions_per_terminal, feature_set_1, feature_set_2, feature_set_3

).drop_index()

print("All the available features:")

all_data.schema.feature_names()

All the available features:

['CUSTOMER_ID',

'TX_AMOUNT',

'TX_FRAUD',

'sum_transactions_7_days',

'count_transactions_7_days',

'sum_transactions_14_days',

'count_transactions_14_days',

'sum_transactions_28_days',

'count_transactions_28_days',

'count_fraud_transactions_7_days',

'rate_fraud_transactions_7_days',

'count_fraud_transactions_14_days',

'rate_fraud_transactions_14_days',

'count_fraud_transactions_28_days',

'rate_fraud_transactions_28_days',

'calendar_hour',

'calendar_day_of_week',

'TERMINAL_ID']

我们提取输入特征的名称。

input_feature_names = [k for k in all_data.schema.feature_names() if k.islower()]

print("The model's input features:")

input_feature_names

The model's input features:

['sum_transactions_7_days',

'count_transactions_7_days',

'sum_transactions_14_days',

'count_transactions_14_days',

'sum_transactions_28_days',

'count_transactions_28_days',

'count_fraud_transactions_7_days',

'rate_fraud_transactions_7_days',

'count_fraud_transactions_14_days',

'rate_fraud_transactions_14_days',

'count_fraud_transactions_28_days',

'rate_fraud_transactions_28_days',

'calendar_hour',

'calendar_day_of_week']

为了让神经网络正常工作,数值输入必须进行归一化。常见的方法是应用 Z-score 归一化,这涉及从训练数据中估计均值和标准差,然后对每个值进行减去均值并除以标准差的操作。在预测中,不建议使用此类 Z-score 归一化,因为它会导致未来数据泄露。具体来说,在时间 t 对交易进行分类时,我们不能依赖时间 t 之后的数据,因为在时间 t 进行预测的服务阶段,尚未有后续数据可用。简而言之,在时间 t,我们仅限于使用时间 t 之前或同时发生的数据。

因此,解决方案是应用基于时间的 Z-score 归一化,这意味着我们使用根据该交易过去数据计算出的均值和标准差来归一化每笔交易。

未来数据泄露是危险的。幸运的是,Temporian 可以提供帮助:唯一可能导致未来数据泄露的操作符是 EventSet.leak()。如果您没有使用 EventSet.leak(),则可以保证您的预处理不会产生未来数据泄露。

注意:对于高级管线,您还可以通过编程方式检查特征是否不依赖于 EventSet.leak() 操作。

# Cast all values (e.g. ints) to floats.

values = all_data[input_feature_names].cast(tp.float32)

# Apply z-normalization overtime.

normalized_features = (

values - values.simple_moving_average(math.inf)

) / values.moving_standard_deviation(math.inf)

# Restore the original name of the features.

normalized_features = normalized_features.rename(values.schema.feature_names())

print(normalized_features)

indexes: []

features: [('sum_transactions_7_days', float32), ('count_transactions_7_days', float32), ('sum_transactions_14_days', float32), ('count_transactions_14_days', float32), ('sum_transactions_28_days', float32), ('count_transactions_28_days', float32), ('count_fraud_transactions_7_days', float32), ('rate_fraud_transactions_7_days', float32), ('count_fraud_transactions_14_days', float32), ('rate_fraud_transactions_14_days', float32), ('count_fraud_transactions_28_days', float32), ('rate_fraud_transactions_28_days', float32), ('calendar_hour', float32), ('calendar_day_of_week', float32)]

events:

(1754155 events):

timestamps: ['2018-04-01T00:00:31' '2018-04-01T00:02:10' '2018-04-01T00:07:56' ...

'2018-09-30T23:58:21' '2018-09-30T23:59:52' '2018-09-30T23:59:57']

'sum_transactions_7_days': [ 0. 1. 1.3636 ... -0.064 -0.2059 0.8428]

'count_transactions_7_days': [ nan nan nan ... 1.0128 0.6892 1.66 ]

'sum_transactions_14_days': [ 0. 1. 1.3636 ... -0.7811 0.156 1.379 ]

'count_transactions_14_days': [ nan nan nan ... 0.2969 0.2969 2.0532]

'sum_transactions_28_days': [ 0. 1. 1.3636 ... -0.7154 -0.2989 1.9396]

'count_transactions_28_days': [ nan nan nan ... 0.1172 -0.1958 1.8908]

'count_fraud_transactions_7_days': [ nan nan nan ... -0.1043 -0.1043 -0.1043]

'rate_fraud_transactions_7_days': [ nan nan nan ... -0.1137 -0.1137 -0.1137]

'count_fraud_transactions_14_days': [ nan nan nan ... -0.1133 -0.1133 0.9303]

'rate_fraud_transactions_14_days': [ nan nan nan ... -0.1216 -0.1216 0.5275]

...

memory usage: 112.3 MB

/home/gbm/my_venv/lib/python3.11/site-packages/temporian/implementation/numpy/operators/binary/arithmetic.py:100: RuntimeWarning: invalid value encountered in divide

return evset_1_feature / evset_2_feature

由于在第一批交易之前只有少量交易,因此它们将使用对均值和标准差的较差估计值进行归一化。为了缓解此问题,我们从训练数据集中移除了第一周的数据。

请注意,第一个值包含 NaN。在 Temporian 中,NaN 代表缺失值,并且所有操作符都会相应地处理它们。例如,在计算移动平均值时,NaN 值不包含在计算中,也不会产生 NaN 结果。

然而,神经网络无法原生处理 NaN 值。因此,我们将它们替换为零。

normalized_features = normalized_features.fillna(0.0)

最后,我们将特征和标签组合在一起。

normalized_all_data = tp.glue(normalized_features, all_data["TX_FRAUD"])

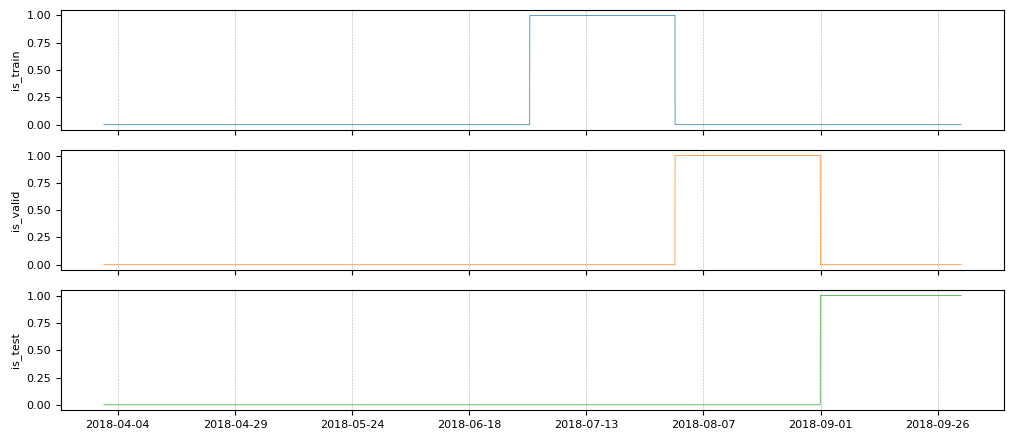

将数据集分割为训练集、验证集和测试集

为了评估我们的机器学习模型的质量,我们需要训练集、验证集和测试集。由于系统是动态的(新的欺诈模式一直在产生),训练集必须在验证集之前,并且验证集必须在测试集之前,这一点很重要。

- 训练集:2018 年 4 月 8 日至 2018 年 7 月 31 日

- 验证集:2018 年 8 月 1 日至 2018 年 8 月 31 日

- 测试集:2018 年 9 月 1 日至 2018 年 9 月 30 日

为了让示例运行更快,我们将有效减小训练集的大小为: - 训练集:2018 年 7 月 1 日至 2018 年 7 月 31 日

# begin_train = datetime.datetime(2018, 4, 8).timestamp() # Full training dataset

begin_train = datetime.datetime(2018, 7, 1).timestamp() # Reduced training dataset

begin_valid = datetime.datetime(2018, 8, 1).timestamp()

begin_test = datetime.datetime(2018, 9, 1).timestamp()

is_train = (normalized_all_data.timestamps() >= begin_train) & (

normalized_all_data.timestamps() < begin_valid

)

is_valid = (normalized_all_data.timestamps() >= begin_valid) & (

normalized_all_data.timestamps() < begin_test

)

is_test = normalized_all_data.timestamps() >= begin_test

is_train、is_valid 和 is_test 是随时间变化的布尔特征,用于指示三个分割部分的界限。让我们绘制它们。

tp.plot(

[

is_train.rename("is_train"),

is_valid.rename("is_valid"),

is_test.rename("is_test"),

]

)

我们在每个分割部分中过滤输入特征和标签。

train_ds_evset = normalized_all_data.filter(is_train)

valid_ds_evset = normalized_all_data.filter(is_valid)

test_ds_evset = normalized_all_data.filter(is_test)

print(f"Training examples: {train_ds_evset.num_events()}")

print(f"Validation examples: {valid_ds_evset.num_events()}")

print(f"Testing examples: {test_ds_evset.num_events()}")

Training examples: 296924

Validation examples: 296579

Testing examples: 288064

在计算特征后分割数据集非常重要,因为训练数据集的一些特征是根据训练窗口期间的交易计算的。

创建 TensorFlow 数据集

我们将数据集从 EventSets 转换为 TensorFlow Datasets,因为 Keras 原生支持它们。

non_batched_train_ds = tp.to_tensorflow_dataset(train_ds_evset)

non_batched_valid_ds = tp.to_tensorflow_dataset(valid_ds_evset)

non_batched_test_ds = tp.to_tensorflow_dataset(test_ds_evset)

使用 TensorFlow 数据集应用以下处理步骤

- 使用

extract_features_and_label将特征和标签分离,格式符合 Keras 的要求。 - 数据集经过分批处理,这意味着示例被分组到 mini-batch 中。

- 训练示例被打乱顺序,以提高 mini-batch 训练的质量。

正如我们之前所指出的,数据集在合法交易方向上存在不平衡。虽然我们希望在此原始分布上评估我们的模型,但神经网络在严重不平衡的数据集上通常训练效果不佳。因此,我们使用 rejection_resample 将训练数据集重采样为 80% 合法 / 20% 欺诈的比例。

def extract_features_and_label(example):

features = {k: example[k] for k in input_feature_names}

labels = tf.cast(example["TX_FRAUD"], tf.int32)

return features, labels

# Target ratio of fraudulent transactions in the training dataset.

target_rate = 0.2

# Number of examples in a mini-batch.

batch_size = 32

train_ds = (

non_batched_train_ds.shuffle(10000)

.rejection_resample(

class_func=lambda x: tf.cast(x["TX_FRAUD"], tf.int32),

target_dist=[1 - target_rate, target_rate],

initial_dist=[1 - fraudulent_rate, fraudulent_rate],

)

.map(lambda _, x: x) # Remove the label copy added by "rejection_resample".

.batch(batch_size)

.map(extract_features_and_label)

.prefetch(tf.data.AUTOTUNE)

)

# The test and validation dataset does not need resampling or shuffling.

valid_ds = (

non_batched_valid_ds.batch(batch_size)

.map(extract_features_and_label)

.prefetch(tf.data.AUTOTUNE)

)

test_ds = (

non_batched_test_ds.batch(batch_size)

.map(extract_features_and_label)

.prefetch(tf.data.AUTOTUNE)

)

WARNING:tensorflow:From /home/gbm/my_venv/lib/python3.11/site-packages/tensorflow/python/data/ops/dataset_ops.py:4956: Print (from tensorflow.python.ops.logging_ops) is deprecated and will be removed after 2018-08-20.

Instructions for updating:

Use tf.print instead of tf.Print. Note that tf.print returns a no-output operator that directly prints the output. Outside of defuns or eager mode, this operator will not be executed unless it is directly specified in session.run or used as a control dependency for other operators. This is only a concern in graph mode. Below is an example of how to ensure tf.print executes in graph mode:

WARNING:tensorflow:From /home/gbm/my_venv/lib/python3.11/site-packages/tensorflow/python/data/ops/dataset_ops.py:4956: Print (from tensorflow.python.ops.logging_ops) is deprecated and will be removed after 2018-08-20.

Instructions for updating:

Use tf.print instead of tf.Print. Note that tf.print returns a no-output operator that directly prints the output. Outside of defuns or eager mode, this operator will not be executed unless it is directly specified in session.run or used as a control dependency for other operators. This is only a concern in graph mode. Below is an example of how to ensure tf.print executes in graph mode:

我们打印训练数据集的前四个示例。这是识别上述可能出现的某些错误的简单方法。

for features, labels in train_ds.take(1):

print("features")

for feature_name, feature_value in features.items():

print(f"\t{feature_name}: {feature_value[:4]}")

print(f"labels: {labels[:4]}")

features

sum_transactions_7_days: [-0.9417254 -1.1157728 -0.5594417 0.7264878]

count_transactions_7_days: [-0.23363686 -0.8702531 -0.23328805 0.7198456 ]

sum_transactions_14_days: [-0.9084115 2.8127224 0.7297886 0.0666021]

count_transactions_14_days: [-0.54289246 2.4122045 0.1963075 0.3798441 ]

sum_transactions_28_days: [-0.44202712 2.3494742 0.20992276 0.97425723]

count_transactions_28_days: [0.02585898 1.8197156 0.12127225 0.9692807 ]

count_fraud_transactions_7_days: [ 8.007475 -0.09783722 1.9282814 -0.09780706]

rate_fraud_transactions_7_days: [14.308702 -0.10952345 1.6929103 -0.10949575]

count_fraud_transactions_14_days: [12.411182 -0.1045466 1.0330476 -0.1045142]

rate_fraud_transactions_14_days: [15.742149 -0.11567765 1.0170861 -0.11565071]

count_fraud_transactions_28_days: [ 7.420907 -0.11298086 0.572011 -0.11293571]

rate_fraud_transactions_28_days: [10.065552 -0.12640427 0.5862939 -0.12637936]

calendar_hour: [-0.68766755 0.6972711 -1.6792761 0.49967623]

calendar_day_of_week: [1.492013 1.4789637 1.4978485 1.4818214]

labels: [1 0 0 0]

Proportion of examples rejected by sampler is high: [0.991630733][0.991630733 0.00836927164][0 1]

Proportion of examples rejected by sampler is high: [0.991630733][0.991630733 0.00836927164][0 1]

Proportion of examples rejected by sampler is high: [0.991630733][0.991630733 0.00836927164][0 1]

Proportion of examples rejected by sampler is high: [0.991630733][0.991630733 0.00836927164][0 1]

Proportion of examples rejected by sampler is high: [0.991630733][0.991630733 0.00836927164][0 1]

Proportion of examples rejected by sampler is high: [0.991630733][0.991630733 0.00836927164][0 1]

Proportion of examples rejected by sampler is high: [0.991630733][0.991630733 0.00836927164][0 1]

Proportion of examples rejected by sampler is high: [0.991630733][0.991630733 0.00836927164][0 1]

Proportion of examples rejected by sampler is high: [0.991630733][0.991630733 0.00836927164][0 1]

Proportion of examples rejected by sampler is high: [0.991630733][0.991630733 0.00836927164][0 1]

训练模型

原始数据集是交易性的,但处理后的数据是表格形式的,仅包含归一化后的数值。因此,我们训练一个前馈神经网络。

inputs = [keras.Input(shape=(1,), name=name) for name in input_feature_names]

x = keras.layers.concatenate(inputs)

x = keras.layers.Dense(32, activation="sigmoid")(x)

x = keras.layers.Dense(16, activation="sigmoid")(x)

x = keras.layers.Dense(1, activation="sigmoid")(x)

model = keras.Model(inputs=inputs, outputs=x)

我们的目标是区分欺诈性和合法性交易,因此我们使用二分类目标。由于数据集不平衡,准确率不是一个有用的指标。相反,我们使用曲线下面积(AUC)来评估模型。

model.compile(

optimizer=keras.optimizers.Adam(0.01),

loss=keras.losses.BinaryCrossentropy(),

metrics=[keras.metrics.Accuracy(), keras.metrics.AUC()],

)

model.fit(train_ds, validation_data=valid_ds)

5/Unknown 1s 15ms/step - accuracy: 0.0000e+00 - auc: 0.4480 - loss: 0.7678

Proportion of examples rejected by sampler is high: [0.991630733][0.991630733 0.00836927164][0 1]

Proportion of examples rejected by sampler is high: [0.991630733][0.991630733 0.00836927164][0 1]

Proportion of examples rejected by sampler is high: [0.991630733][0.991630733 0.00836927164][0 1]

Proportion of examples rejected by sampler is high: [0.991630733][0.991630733 0.00836927164][0 1]

Proportion of examples rejected by sampler is high: [0.991630733][0.991630733 0.00836927164][0 1]

Proportion of examples rejected by sampler is high: [0.991630733][0.991630733 0.00836927164][0 1]

Proportion of examples rejected by sampler is high: [0.991630733][0.991630733 0.00836927164][0 1]

Proportion of examples rejected by sampler is high: [0.991630733][0.991630733 0.00836927164][0 1]

Proportion of examples rejected by sampler is high: [0.991630733][0.991630733 0.00836927164][0 1]

Proportion of examples rejected by sampler is high: [0.991630733][0.991630733 0.00836927164][0 1]

433/Unknown 23s 51ms/step - accuracy: 0.0000e+00 - auc: 0.8060 - loss: 0.3632

/usr/lib/python3.11/contextlib.py:155: UserWarning: Your input ran out of data; interrupting training. Make sure that your dataset or generator can generate at least `steps_per_epoch * epochs` batches. You may need to use the `.repeat()` function when building your dataset.

self.gen.throw(typ, value, traceback)

433/433 ━━━━━━━━━━━━━━━━━━━━ 30s 67ms/step - accuracy: 0.0000e+00 - auc: 0.8060 - loss: 0.3631 - val_accuracy: 0.0000e+00 - val_auc: 0.8252 - val_loss: 0.2133

<keras.src.callbacks.history.History at 0x7f8f74f0d750>

我们在测试数据集上评估模型。

model.evaluate(test_ds)

9002/9002 ━━━━━━━━━━━━━━━━━━━━ 7s 811us/step - accuracy: 0.0000e+00 - auc: 0.8357 - loss: 0.2161

[0.2171599417924881, 0.0, 0.8266682028770447]

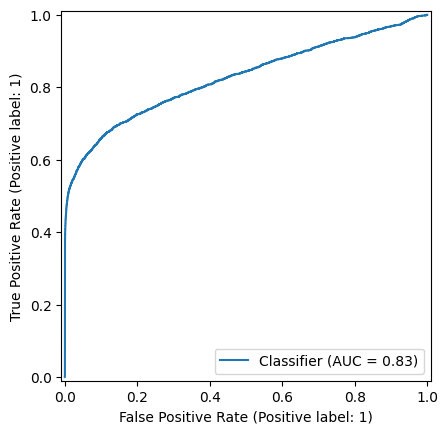

AUC 约为 83%,我们的简单欺诈检测器显示出令人鼓舞的结果。

绘制 ROC 曲线是一个很好的解决方案,可以帮助理解和选择模型的操作点,即应用于模型输出以区分欺诈性交易和合法性交易的阈值。

计算测试预测结果

predictions = model.predict(test_ds)

predictions = np.nan_to_num(predictions, nan=0)

9002/9002 ━━━━━━━━━━━━━━━━━━━━ 10s 1ms/step

从测试集中提取标签

labels = np.concatenate([label for _, label in test_ds])

最后,我们绘制 ROC 曲线。

_ = RocCurveDisplay.from_predictions(labels, predictions)

该 Keras 模型已准备好用于处理欺诈状态未知的交易,即服务阶段。我们将模型保存到磁盘以备将来使用。

注意:该模型不包含在 Pandas 和 Temporian 中完成的数据准备和预处理步骤。必须手动将这些步骤应用于输入到模型的数据。虽然此处未演示,但 Temporian 预处理也可以使用 tp.save 保存到磁盘。

model.save("fraud_detection_model.keras")

稍后可以使用以下方式重新加载模型

loaded_model = keras.saving.load_model("fraud_detection_model.keras")

# Generate predictions with the loaded model on 5 test examples.

loaded_model.predict(test_ds.rebatch(5).take(1))

1/1 ━━━━━━━━━━━━━━━━━━━━ 0s 71ms/step

/usr/lib/python3.11/contextlib.py:155: UserWarning: Your input ran out of data; interrupting training. Make sure that your dataset or generator can generate at least `steps_per_epoch * epochs` batches. You may need to use the `.repeat()` function when building your dataset.

self.gen.throw(typ, value, traceback)

array([[0.08197185],

[0.16517264],

[0.13180313],

[0.10209075],

[0.14283912]], dtype=float32)

结论

我们训练了一个前馈神经网络来识别欺诈性交易。为了将它们输入到模型中,交易使用 Temporian 进行了预处理并转换成了表格数据集。现在,留给读者一个问题:还可以采取哪些措施来进一步提高模型的性能?

以下是一些建议

- 在整个数据集上训练模型,而不是仅使用一个月的数据。

- 训练模型更多个 epochs,并使用早停机制确保模型充分训练且不过拟合。

- 通过增加层数来增强前馈网络的性能,同时确保模型经过正则化处理。

- 计算额外的预处理特征。例如,除了按终端聚合交易外,还可以按客户聚合交易。

- 使用 Keras Tuner 对模型进行超参数调优。请注意,预处理的参数(例如,聚合的天数)也是可以调优的超参数。