无

用于客户终身价值的深度学习

作者: Praveen Hosdrug

创建日期 2024/11/23

最后修改日期 2024/11/27

描述: 一个混合深度学习架构,用于预测客户购买模式和生命周期价值。

简介

一个混合深度学习架构,结合了 Transformer 编码器和 LSTM 网络,利用交易历史来预测客户购买模式和生命周期价值。虽然许多现有的评论文章都侧重于经典的参数模型和传统机器学习算法,但本实现利用了 Transformer 模型在时间序列预测方面的最新进展。该方法能够处理跨不同时间尺度的多粒度预测。

为深度学习项目设置库

import subprocess

def install_packages(packages):

"""

Install a list of packages using pip.

Args:

packages (list): A list of package names to install.

"""

for package in packages:

subprocess.run(["pip", "install", package], check=True)

要安装的软件包列表

- uciml:在本教程中;我们将使用英国零售 数据集

- keras_hub:访问 Transformer 编码器层。

packages_to_install = ["ucimlrepo", "keras_hub"]

# Install the packages

install_packages(packages_to_install)

# Core data processing and numerical libraries

import os

os.environ["KERAS_BACKEND"] = "jax"

import keras

import numpy as np

import pandas as pd

from typing import Dict

# Visualization

import matplotlib.pyplot as plt

# Keras imports

from keras import layers

from keras import Model

from keras import ops

from keras_hub.layers import TransformerEncoder

from keras import regularizers

# UK Retail Dataset

from ucimlrepo import fetch_ucirepo

预处理英国零售数据集

def prepare_time_series_data(data):

"""

Preprocess retail transaction data for deep learning.

Args:

data: Raw transaction data containing InvoiceDate, UnitPrice, etc.

Returns:

Processed DataFrame with calculated features

"""

processed_data = data.copy()

# Essential datetime handling for temporal ordering

processed_data["InvoiceDate"] = pd.to_datetime(processed_data["InvoiceDate"])

# Basic business constraints and calculations

processed_data = processed_data[processed_data["UnitPrice"] > 0]

processed_data["Amount"] = processed_data["UnitPrice"] * processed_data["Quantity"]

processed_data["CustomerID"] = processed_data["CustomerID"].fillna(99999.0)

# Handle outliers in Amount using statistical thresholds

q1 = processed_data["Amount"].quantile(0.25)

q3 = processed_data["Amount"].quantile(0.75)

# Define bounds - using 1.5 IQR rule

lower_bound = q1 - 1.5 * (q3 - q1)

upper_bound = q3 + 1.5 * (q3 - q1)

# Filter outliers

processed_data = processed_data[

(processed_data["Amount"] >= lower_bound)

& (processed_data["Amount"] <= upper_bound)

]

return processed_data

# Load Data

online_retail = fetch_ucirepo(id=352)

raw_data = online_retail.data.features

transformed_data = prepare_time_series_data(raw_data)

def prepare_data_for_modeling(

df: pd.DataFrame,

input_sequence_length: int = 6,

output_sequence_length: int = 6,

) -> Dict:

"""

Transform retail data into sequence-to-sequence format with separate

temporal and trend components.

"""

df = df.copy()

# Daily aggregation

daily_purchases = (

df.groupby(["CustomerID", pd.Grouper(key="InvoiceDate", freq="D")])

.agg({"Amount": "sum", "Quantity": "sum", "Country": "first"})

.reset_index()

)

daily_purchases["frequency"] = np.where(daily_purchases["Amount"] > 0, 1, 0)

# Monthly resampling

monthly_purchases = (

daily_purchases.set_index("InvoiceDate")

.groupby("CustomerID")

.resample("M")

.agg(

{"Amount": "sum", "Quantity": "sum", "frequency": "sum", "Country": "first"}

)

.reset_index()

)

# Add cyclical temporal features

def prepare_temporal_features(input_window: pd.DataFrame) -> np.ndarray:

month = input_window["InvoiceDate"].dt.month

month_sin = np.sin(2 * np.pi * month / 12)

month_cos = np.cos(2 * np.pi * month / 12)

is_quarter_start = (month % 3 == 1).astype(int)

temporal_features = np.column_stack(

[

month,

input_window["InvoiceDate"].dt.year,

month_sin,

month_cos,

is_quarter_start,

]

)

return temporal_features

# Prepare trend features with lagged values

def prepare_trend_features(input_window: pd.DataFrame, lag: int = 3) -> np.ndarray:

lagged_data = pd.DataFrame()

for i in range(1, lag + 1):

lagged_data[f"Amount_lag_{i}"] = input_window["Amount"].shift(i)

lagged_data[f"Quantity_lag_{i}"] = input_window["Quantity"].shift(i)

lagged_data[f"frequency_lag_{i}"] = input_window["frequency"].shift(i)

lagged_data = lagged_data.fillna(0)

trend_features = np.column_stack(

[

input_window["Amount"].values,

input_window["Quantity"].values,

input_window["frequency"].values,

lagged_data.values,

]

)

return trend_features

sequence_containers = {

"temporal_sequences": [],

"trend_sequences": [],

"static_features": [],

"output_sequences": [],

}

# Process sequences for each customer

for customer_id, customer_data in monthly_purchases.groupby("CustomerID"):

customer_data = customer_data.sort_values("InvoiceDate")

sequence_ranges = (

len(customer_data) - input_sequence_length - output_sequence_length + 1

)

country = customer_data["Country"].iloc[0]

for i in range(sequence_ranges):

input_window = customer_data.iloc[i : i + input_sequence_length]

output_window = customer_data.iloc[

i

+ input_sequence_length : i

+ input_sequence_length

+ output_sequence_length

]

if (

len(input_window) == input_sequence_length

and len(output_window) == output_sequence_length

):

temporal_features = prepare_temporal_features(input_window)

trend_features = prepare_trend_features(input_window)

sequence_containers["temporal_sequences"].append(temporal_features)

sequence_containers["trend_sequences"].append(trend_features)

sequence_containers["static_features"].append(country)

sequence_containers["output_sequences"].append(

output_window["Amount"].values

)

return {

"temporal_sequences": (

np.array(sequence_containers["temporal_sequences"], dtype=np.float32)

),

"trend_sequences": (

np.array(sequence_containers["trend_sequences"], dtype=np.float32)

),

"static_features": np.array(sequence_containers["static_features"]),

"output_sequences": (

np.array(sequence_containers["output_sequences"], dtype=np.float32)

),

}

# Transform data with input and output sequences into a Output dictionary

output = prepare_data_for_modeling(

df=transformed_data, input_sequence_length=6, output_sequence_length=6

)

/var/folders/28/qvxw5wfs4b7gzvxt7_xp20640000gn/T/ipykernel_26202/277084066.py:66: FutureWarning: 'M' is deprecated and will be removed in a future version, please use 'ME' instead.

daily_purchases.set_index("InvoiceDate")

缩放和拆分

def robust_scale(data):

"""

Min-Max scaling function since standard deviation is high.

"""

data = np.array(data)

data_min = np.min(data)

data_max = np.max(data)

scaled = (data - data_min) / (data_max - data_min)

return scaled

def create_temporal_splits_with_scaling(

prepared_data: Dict[str, np.ndarray],

test_ratio: float = 0.2,

val_ratio: float = 0.2,

):

total_sequences = len(prepared_data["trend_sequences"])

# Calculate split points

test_size = int(total_sequences * test_ratio)

val_size = int(total_sequences * val_ratio)

train_size = total_sequences - (test_size + val_size)

# Scale trend sequences

trend_shape = prepared_data["trend_sequences"].shape

scaled_trends = np.zeros_like(prepared_data["trend_sequences"])

# Scale each feature independently

for i in range(trend_shape[-1]):

scaled_trends[..., i] = robust_scale(prepared_data["trend_sequences"][..., i])

# Scale output sequences

scaled_outputs = robust_scale(prepared_data["output_sequences"])

# Create splits

train_data = {

"trend_sequences": scaled_trends[:train_size],

"temporal_sequences": prepared_data["temporal_sequences"][:train_size],

"static_features": prepared_data["static_features"][:train_size],

"output_sequences": scaled_outputs[:train_size],

}

val_data = {

"trend_sequences": scaled_trends[train_size : train_size + val_size],

"temporal_sequences": prepared_data["temporal_sequences"][

train_size : train_size + val_size

],

"static_features": prepared_data["static_features"][

train_size : train_size + val_size

],

"output_sequences": scaled_outputs[train_size : train_size + val_size],

}

test_data = {

"trend_sequences": scaled_trends[train_size + val_size :],

"temporal_sequences": prepared_data["temporal_sequences"][

train_size + val_size :

],

"static_features": prepared_data["static_features"][train_size + val_size :],

"output_sequences": scaled_outputs[train_size + val_size :],

}

return train_data, val_data, test_data

# Usage

train_data, val_data, test_data = create_temporal_splits_with_scaling(output)

评估

def calculate_metrics(y_true, y_pred):

"""

Calculates RMSE, MAE and R²

"""

# Convert inputs to "float32"

y_true = ops.cast(y_true, dtype="float32")

y_pred = ops.cast(y_pred, dtype="float32")

# RMSE

rmse = np.sqrt(np.mean(np.square(y_true - y_pred)))

# R² (coefficient of determination)

ss_res = np.sum(np.square(y_true - y_pred))

ss_tot = np.sum(np.square(y_true - np.mean(y_true)))

r2 = 1 - (ss_res / ss_tot)

return {"mae": np.mean(np.abs(y_true - y_pred)), "rmse": rmse, "r2": r2}

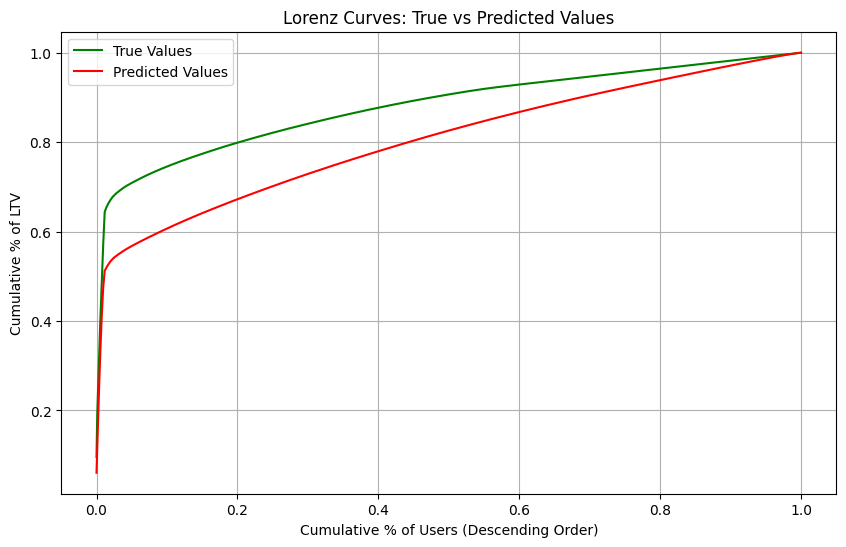

def plot_lorenz_analysis(y_true, y_pred):

"""

Plots Lorenz curves to show distribution of high and low value users

"""

# Convert to numpy arrays and flatten

y_true = np.array(y_true).flatten()

y_pred = np.array(y_pred).flatten()

# Sort values in descending order (for high-value users analysis)

true_sorted = np.sort(-y_true)

pred_sorted = np.sort(-y_pred)

# Calculate cumulative sums

true_cumsum = np.cumsum(true_sorted)

pred_cumsum = np.cumsum(pred_sorted)

# Normalize to percentages

true_cumsum_pct = true_cumsum / true_cumsum[-1]

pred_cumsum_pct = pred_cumsum / pred_cumsum[-1]

# Generate percentiles for x-axis

percentiles = np.linspace(0, 1, len(y_true))

# Calculate Mutual Gini (area between curves)

mutual_gini = np.abs(

np.trapz(true_cumsum_pct, percentiles) - np.trapz(pred_cumsum_pct, percentiles)

)

# Create plot

plt.figure(figsize=(10, 6))

plt.plot(percentiles, true_cumsum_pct, "g-", label="True Values")

plt.plot(percentiles, pred_cumsum_pct, "r-", label="Predicted Values")

plt.xlabel("Cumulative % of Users (Descending Order)")

plt.ylabel("Cumulative % of LTV")

plt.title("Lorenz Curves: True vs Predicted Values")

plt.legend()

plt.grid(True)

print(f"\nMutual Gini: {mutual_gini:.4f} (lower is better)")

plt.show()

return mutual_gini

混合 Transformer / LSTM 模型架构

该模型的混合性质尤其重要,因为它结合了 RNN 处理序列数据的能力与 Transformer 的注意力机制,以捕捉跨国家和季节性的全局模式。

def build_hybrid_model(

input_sequence_length: int,

output_sequence_length: int,

num_countries: int,

d_model: int = 8,

num_heads: int = 4,

):

keras.utils.set_random_seed(seed=42)

# Inputs

temporal_inputs = layers.Input(

shape=(input_sequence_length, 5), name="temporal_inputs"

)

trend_inputs = layers.Input(shape=(input_sequence_length, 12), name="trend_inputs")

country_inputs = layers.Input(

shape=(num_countries,), dtype="int32", name="country_inputs"

)

# Process country features

country_embedding = layers.Embedding(

input_dim=num_countries,

output_dim=d_model,

mask_zero=False,

name="country_embedding",

)(

country_inputs

) # Output shape: (batch_size, 1, d_model)

# Flatten the embedding output

country_embedding = layers.Flatten(name="flatten_country_embedding")(

country_embedding

)

# Repeat the country embedding across timesteps

country_embedding_repeated = layers.RepeatVector(

input_sequence_length, name="repeat_country_embedding"

)(country_embedding)

# Projection of temporal inputs to match Transformer dimensions

temporal_projection = layers.Dense(

d_model, activation="tanh", name="temporal_projection"

)(temporal_inputs)

# Combine all features

combined_features = layers.Concatenate()(

[temporal_projection, country_embedding_repeated]

)

transformer_output = combined_features

for _ in range(3):

transformer_output = TransformerEncoder(

intermediate_dim=16, num_heads=num_heads

)(transformer_output)

lstm_output = layers.LSTM(units=64, name="lstm_trend")(trend_inputs)

transformer_flattened = layers.GlobalAveragePooling1D(name="flatten_transformer")(

transformer_output

)

transformer_flattened = layers.Dense(1, activation="sigmoid")(transformer_flattened)

# Concatenate flattened Transformer output with LSTM output

merged_features = layers.Concatenate(name="concatenate_transformer_lstm")(

[transformer_flattened, lstm_output]

)

# Repeat the merged features to match the output sequence length

decoder_initial = layers.RepeatVector(

output_sequence_length, name="repeat_merged_features"

)(merged_features)

decoder_lstm = layers.LSTM(

units=64,

return_sequences=True,

recurrent_regularizer=regularizers.L1L2(l1=1e-5, l2=1e-4),

)(decoder_initial)

# Output Dense layer

output = layers.Dense(units=1, activation="linear", name="output_dense")(

decoder_lstm

)

model = Model(

inputs=[temporal_inputs, trend_inputs, country_inputs], outputs=output

)

model.compile(

optimizer=keras.optimizers.Adam(learning_rate=0.001),

loss="mse",

metrics=["mse"],

)

return model

# Create the hybrid model

model = build_hybrid_model(

input_sequence_length=6,

output_sequence_length=6,

num_countries=len(np.unique(train_data["static_features"])) + 1,

d_model=8,

num_heads=4,

)

# Configure StringLookup

label_encoder = layers.StringLookup(output_mode="one_hot", num_oov_indices=1)

# Adapt and encode

label_encoder.adapt(train_data["static_features"])

train_static_encoded = label_encoder(train_data["static_features"])

val_static_encoded = label_encoder(val_data["static_features"])

test_static_encoded = label_encoder(test_data["static_features"])

# Convert sequences with proper type casting

x_train_seq = np.asarray(train_data["trend_sequences"]).astype(np.float32)

x_val_seq = np.asarray(val_data["trend_sequences"]).astype(np.float32)

x_train_temporal = np.asarray(train_data["temporal_sequences"]).astype(np.float32)

x_val_temporal = np.asarray(val_data["temporal_sequences"]).astype(np.float32)

train_outputs = np.asarray(train_data["output_sequences"]).astype(np.float32)

val_outputs = np.asarray(val_data["output_sequences"]).astype(np.float32)

test_output = np.asarray(test_data["output_sequences"]).astype(np.float32)

# Training setup

keras.utils.set_random_seed(seed=42)

history = model.fit(

[x_train_temporal, x_train_seq, train_static_encoded],

train_outputs,

validation_data=(

[x_val_temporal, x_val_seq, val_static_encoded],

val_data["output_sequences"].astype(np.float32),

),

epochs=20,

batch_size=30,

)

# Make predictions

predictions = model.predict(

[

test_data["temporal_sequences"].astype(np.float32),

test_data["trend_sequences"].astype(np.float32),

test_static_encoded,

]

)

# Calculate the predictions

predictions = np.squeeze(predictions)

# Calculate basic metrics

hybrid_metrics = calculate_metrics(test_data["output_sequences"], predictions)

# Plot Lorenz curves and get Mutual Gini

hybrid_mutual_gini = plot_lorenz_analysis(test_data["output_sequences"], predictions)

Mutual Gini: 0.0759 (lower is better)

/var/folders/28/qvxw5wfs4b7gzvxt7_xp20640000gn/T/ipykernel_26202/1632064435.py:45: DeprecationWarning: `trapz` is deprecated. Use `trapezoid` instead, or one of the numerical integration functions in `scipy.integrate`.

np.trapz(true_cumsum_pct, percentiles) - np.trapz(pred_cumsum_pct, percentiles)

结论

虽然 LSTMs 在序列到序列学习方面表现出色,如 Sutskever, I., Vinyals, O., & Le, Q. V. (2014) Sequence to sequence learning with neural networks. 一文所示,这里的混合方法在此基础上进行了增强。注意力机制的增加允许模型在保持 LSTM 固有的序列学习优势的同时,自适应地关注相关的时间/地理模式。正如 Zhou, H., Zhang, S., Peng, J., Zhang, S., Li, J., Xiong, H., & Zhang, W. (2021) 的 Informer: Beyond Efficient Transformer for Long Sequence Time-Series Forecasting 一文所证明的,这种组合在处理时间序列预测中的周期性模式和特殊事件方面尤其有效。